The Software-Defined Vehicle: Impacts Across the Automotive Ecosystem

This is the era of the software-defined vehicle (SDV) — an evolution in the way vehicles are designed, built, and maintained, now and into the future. This is also a time for unprecedented collaboration with distinct yet interdependent players across the automotive, technology and communications industries. Together, they are all working to develop transformative new models for delivering value to mobility customers.

Key to understanding the term software-defined vehicle is recognizing that, for over 100 years, innovation within the automotive industry has been harnessed primarily through hardware and electro-mechanical features like torque and horsepower. Now, solutions are arriving from a very different direction, with lines of code and digital platforms being primary drivers of differentiation for manufacturers bringing their next-generation vehicles to market.

Software controls an increasing range of systems across today's vehicles, including cutting-edge advanced driver assistance (ADAS) features. Software also underpins the cloud-based connectivity platforms enabling over-the-air (OTA) updates and the ever-upgradeable, seamless delivery of additional services and digital cabin experiences. This has turned vehicle and systems development completely upside down.

Introducing new features — decoupled from the hardware development cycle — means that electronics architecture and hardware must now be designed to support the software, not the other way around. This applies not just to advanced connectivity or ADAS features, but also to every system in the car, including steering, braking, propulsion, etc.

The Software-Defined Vehicle’s Changing Landscape

The industry’s shift to the SDV anchors the consumer at the center of an evolving new ecosystem. This is an environment less defined by static, model-year upgrades than by collaborative efforts to facilitate continuous improvement and optimize the customer experience.

As hardware platforms become increasingly standardized, other elements required for the ecosystem — like the low latency and real-time connectivity provided by 5G, plus vehicle-to-everything (V2X) infrastructure — are also falling into place. This further pivots the focus to software, particularly how to leverage software’s capabilities for future-proofing products and better support customer’s wants and needs.

The advanced connectivity embedded into today's and tomorrow’s SDV provides invaluable engagement for building long-term brand loyalty that is based not just on product performance, but service and customer experiences as well.

Differentiation through software offers automotive manufacturers (OEMs) an invaluable opportunity to mold and define exceptional cockpit experiences while also ensuring seamless availability to the unique digital worlds of all passengers in the car. “Always on,” two-way connectivity provides seamless monitoring, analysis and control of user experience. It also opens a lane for future revenue streams.

When you realize that answering the questions (1) How do we keep the software fresh? and (2) How do we keep the customer experience fresh? sets you upon parallel, if not identical, paths, then it’s clear how integral and vital software (and its engineers!) have become to the industry.

Numerous other questions remain to be addressed as the SDV era unfolds. For example, who ultimately controls the user experience and the valuable data produced by the software-defined vehicle?

An Evolving Ecosystem for the Software-Defined Vehicle

While the transition to SDVs impacts the industry’s traditional players and their way of doing business, we see newer, digital-native participants finding their own footing as well. The critical challenge for OEMs is navigating to the most strategic balance between in-house control and the external partnerships that offer value in areas outside their own expertise.

How these choices, trade-offs and alliances play out will have implications up and down the value chain. Here’s a brief overview of how the ecosystem may evolve as roles shift in the forging of a dynamic, new collaborative model.

Automotive & Mobility Ecosystem Participants' Changing Roles

Consumer

At the center of the ecosystem sits the consumer (drivers and passengers) for whom all other ecosystem participants focus the delivery of their solutions. In some instances, they may not even be the purchaser or owner of the vehicle, as emergent models, such as shared mobility, gain more traction.

Car Maker

The vehicle manufacturer (OEM), however, will still function as the de facto “car maker,” providing vehicle design, development, delivery and support. In this way, the traditional role of the OEM remains the same: the owner and steward of the customer relationship.

In addition to offering alternative “ownership” models, (e.g., sharing and subscriptions) and providing open platforms for third-party services, the OEM will increasingly become a software system integrator. Specifically, OEMs will integrate externally sourced software innovations into their car operating system and compute platforms.

All other participants in the ecosystem will be vying for traction and delivery of their unique, and sometimes overlapping, solutions in what ideally will be a network of open, collaborative partnerships. As potential turf battles work towards resolution, new business models are likely to evolve, recognizing the redrawn contours of risk and reward across the industry.

Mobility Services Provider

According to Frost & Sullivan’s “Mobility and Other Downstream Services Market, Forecast to 2030,” revenues from connected mobility markets such as carsharing, ride-hailing, shuttles and multi-modal mobility-as-a-service platforms are expected to reach $2 trillion by 2030.

The scale of this number reinforces an undeniable paradigm shift for the industry in which mobility is consumed less as a product than as a service. As this trajectory continues — reduced individual vehicle ownership and more shared mobility, like ride-hailing, robo-taxis, etc. — then the vehicle brand is likely to diminish in importance, particularly for consumers in dense, urban settings.

Solving for the simplest and least expensive way to get from point A to point B has been central to the industry’s calculus from the beginning. The era of the SDV welcomes a range of exciting new ways to address personal mobility. How it plays out, ultimately, is something for the consumer to decide.

Cloud Services Provider

Cloud services provider opportunities will continue to build off their role as the owner and/or manager of OTA updates and the host of artificial intelligence (AI)-driven platforms and vehicle digital twins. They are positioned literally at the gateway between data processing and service delivery — the heart of the SDV platform model.

Low-latency, high-bandwidth information exchange has the potential to revolutionize the roads with truly “smart” systems whose impact will save lives, reduce road congestion and promote more sustainable modes of travel.

Increasingly sophisticated consumer services (e.g., a voice controlled digital assistant like Alexa but in the car) are a natural extension for cloud service providers’ value-add. Making these consumer and mobility relevant services integrable into or accessible from the “Car OS” should be a priority at this edge of the ecosystem.

Software Providers

Integrability is likewise a priority for developers of software mapped for the SDV.

Imagine the SDV as a data center on wheels — a platform coordinating the complex communications of internal and external compute over high-speed networks. Looked at through this lens, it is clear that software products need to be defined with standardized, interoperable interfaces.

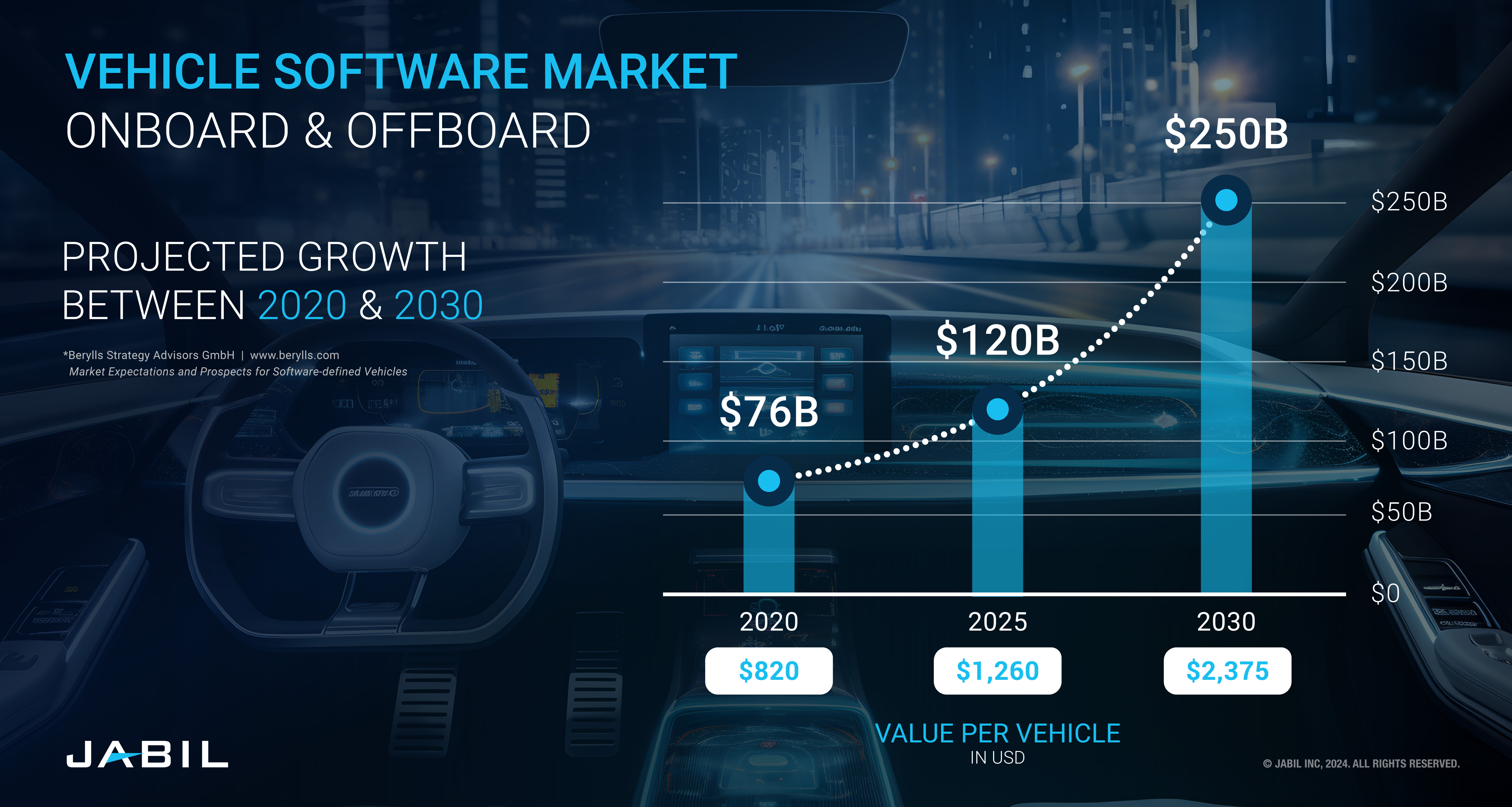

Automated diagnostics and OTA updates, real-time performance optimization, and proactive security are a few of the baseline requirements for the SDV. The market for enabling and future-proofing these capabilities through software is projected by Berylls Strategy Advisors (see accompanying graphic) to accelerate dramatically through the end of the decade, topping $250 billion by 2030.

The global automotive and mobility industry consultants analyzed a range of software sub-segments for their detailed study (released in 2021), including connected services, infotainment, driving experience, and security integration, certification and validation software. In addition to projecting significant growth in the ADAS and autonomous driving domain, high-performance computing (HPC) software is also expected to deliver double-digit compound annual growth between now and 2030 due to changing vehicle architectures and the increasing centralization of processing power.

Any comprehensive value analysis of software providers’ impact upon the industry should, however, extend beyond revenues. As architects of the consumer experience, their growth trajectory is limited only by imagination as the industry continues its evolution from producing product to delivering service.

Supporting Services, Vendors and Suppliers

The remaining ecosystem participants are less likely to be the primary holders of intellectual property (IP) and aligned more towards roles defined by facilitation and support. Their influence and impact within the ecosystem are a matter to be determined as the software-defined vehicle era unfolds.

Engineering Services

Engineering services will find traction where the mobility service provider or vehicle OEM lacks appropriate engineering skills or capacity in-house. Hardware and software designs will still be owned and controlled by the OEM, but as complexity increases, there’s significant value in partnering with external resources dedicated to, for instance, product testing and validation, rather than maintaining those services in-house.

Semiconductor Vendors

Likewise, semiconductor vendors will continue to provide OEMs and mobility service providers reference designs, development boards and system-on-chip (SoC) designs as vehicle architectures continue to evolve. Whether it’s ADAS today or autonomous driving tomorrow, SDVs need powerful state-of-the-art semiconductor devices to run the complex algorithms and process the billions of operations per second required for advanced vehicle performance.

Tier-One Suppliers

Tier-one suppliers will be expected to take on ever more complex system integration and sub-system integration responsibilities while continuing to support OEMs and mobility service providers with hardware and software design services. Ownership of IP will not likely reside within their sphere, although there will be increased opportunities for tier-ones to compete for build-to-print, manufacturing-only business models.

Tier-Two Suppliers

No longer tied directly to the tier-ones, tier-two suppliers will be looking to find traction within a broader field of operation achieving component design wins and sourcing.

In-house design teams within mobility providers and OEMs, as well as engineering services and contract manufacturers all have potential for developing synergistic value in partnership with tier-two suppliers.

Contract Manufacturers

For contract manufacturers (CMs), the changing automotive landscape offers tremendous upside for those firms able to deliver specialized services, technical expertise, and supply chain scale and optimization.

As an agent of commercialization efficiency and process management, CMs can significantly reduce the time required for mass-production processes, whether it’s introducing new lines or scaling up existing ones. When these benefits are combined with cost-saving product management and design services — as well as a global production and procurement footprint with outstanding supply chain visibility — the results are improved efficiency, lower costs and more robust, resilient margins.

Any or all of these advantages from a CM can be tapped to support the other ecosystem participants with hardware design services and manufacturing of technical solutions.

The Software-Defined Road Ahead

In addition to the vast and complex technical requirements of the emerging software-defined vehicle, supply chains and production networks are so complex that no single OEM or mobility services company can rely on the old models and enjoy their past success. The way forward is through partnerships of complementary specialists and flexibility to adapt to the changing landscape.

Economics and time-to-market pressures will continue to power the way forward while shaping how the market's new demands are realized. In the meantime, there is one thing all the participants in the ecosystem can agree on: The SDV model is an exceptional way to accommodate complexity and facilitate innovation in a constantly evolving and rapid paced world.

How can Jabil help you meet your software-defined vehicle goals? Contact us.

No matter how complex or demanding the project, we’re helping today’s innovators solve it. Get started with a trusted partner.