Scaling Robotics and Physical AI in North America: The Market is Ready. Is Your Manufacturing Strategy?

Apr 10, 2026

Look out across a modern fulfillment center, and the scale of what warehouse automation makes possible comes strikingly into focus.

Autonomous mobile robots (AMRs) navigate defined pathways. Robotic arms equipped with 3D vision systems, and specialized grippers sort mixed SKUs with sub-millimeter precision. AI-driven conveyor systems work in tandem with robotics, cloud computing, and other automated technologies.

Across these increasingly intelligent systems, human workers oversee workflows, intervene when exceptions arise, and continuously optimize throughput, safety, and quality. Meanwhile, advances in physical AI are expanding automation’s reach: humanoid robots are becoming increasingly dexterous, and beyond the warehouse floor, drone fleets are rewriting the economics of last-mile delivery.

The scenes described here are neither experimental nor aspirational. They are operational today, across fulfillment centers, manufacturing environments, and last-mile networks run by some of the world’s largest retailers and logistics providers. Yet beyond the early adopters, scale remains uneven. As automation expands across retail, food delivery, manufacturing, and commercial kitchens, the imperative to get leaner and faster intensifies. The business case is settled. Capital is flowing. Physical AI has moved from pilot to production. And the capability ceiling is rising faster than most industry forecasts anticipated.

Despite this momentum, scaled North American deployments have not kept pace with demand. A gap has opened between strategic intent and operational execution. Until it is closed, companies competing in this sector risk slower revenue realization, margin compression, and stranded capital in markets that reward speed and operational efficiency.

Three structural barriers continue to slow the sector’s ability to scale, challenges many OEMs cannot afford to overlook.

1. Regulatory and Trade Complexity

The rules governing where and how robotics systems are built are changing — and quickly. Trade policy, geopolitical tension, and supply chain risk now shape automation strategy as decisively as technological capability.

Global supply chains once optimized primarily for cost are being reassessed for resilience and regional alignment. If the lessons from COVID were to build resilience into potentially fragile offshore supply chains, then the current moment is an intensive refresher course. Shifting trade dynamics between China and Western economies and broader geopolitical uncertainty continue to reinforce that message.

Much of the robotics supply chain — from rare earth magnets and precision motors to sensors and power electronics — remains heavily concentrated in Asia. China alone processes more than 90% of the world’s rare earth magnets, a critical input for advanced robotics motors. As a result, Western manufacturers are under growing pressure to localize or diversify production. Dual sourcing, once optional, is increasingly viewed as essential, even when it carries higher upfront cost.

Rebuilding robotics supply chains in-region will not happen overnight, but the direction is clear. Capital — both private and public — is beginning to follow. In the United States, constructive policy is emerging. The National Commission on Robotics Act, introduced in February 2026, aims to strengthen U.S. leadership in robotics manufacturing and provide a roadmap for reshoring production while maintaining a technological edge.

At the same time, trade frameworks such as the U.S.-Mexico-Canada Agreement (USMCA) offer meaningful advantages, but only for companies that understand what qualification truly requires. It is not simply a matter of where final assembly occurs. Content transformation thresholds, origin qualification, and supply chain documentation must be deliberately architected into the production strategy from the outset. Treating compliance as a box to check underestimates not only the complexity, but the opportunity.

The broader tariff environment adds another layer of uncertainty. Ongoing fluctuations in trade policy introduce meaningful cost exposure for OEMs with components or subassemblies sourced from Asia. When trade rules are in flux, cautious companies often hesitate. Hesitation slows decision-making. And delay erodes competitive advantage. In a sector where first-mover advantage can be decisive, the ability to stay ahead of regulatory change becomes a strategic capability in its own right.

2. Capital Intensity and Infrastructure Risk

Building a manufacturing facility from scratch to produce robotics hardware in the United States is expensive, slow, and carries enormous fixed-cost risk. Standing up a purpose-built plant requires years of capital commitment, long lead times for buildout and tooling, and ongoing operating overhead. It should also be noted that all of this has to be taken on at exactly the moment when the underlying product technology is evolving fastest.

This creates a particularly uncomfortable dynamic for physical AI companies. The products seeing explosive demand growth — like AMRs, humanoid platforms, autonomous delivery systems — are also the products with the fastest development cycles. Committing to fixed infrastructure built around today's product configuration is a significant bet that tomorrow's version will not require meaningfully different manufacturing capabilities. In a sector defined by rapid iteration, that is a bet that carries real risk.

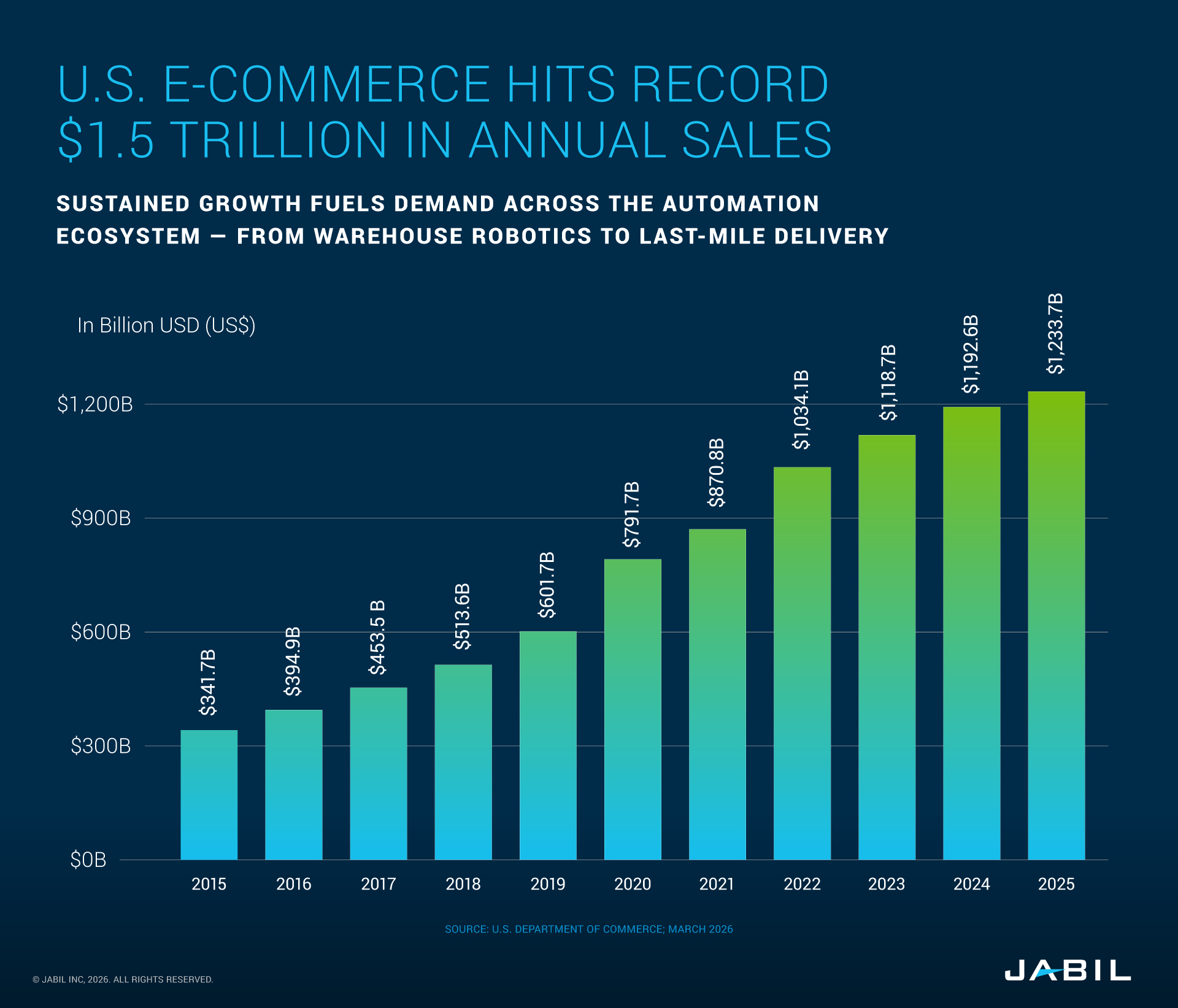

The scale of the market these systems are being built to serve makes the capital efficiency argument even more pressing. According to the U.S. Census Bureau, e-commerce accounted for approximately 16.4% of total U.S. retail sales in the third quarter of 2025, representing more than $310 billion and growing at roughly 5% year over year. Globally, more than 400 billion packages shipped in 2025, with nearly 500 billion projected by 2028. Missing a market window in this environment is a hard error to recover from.

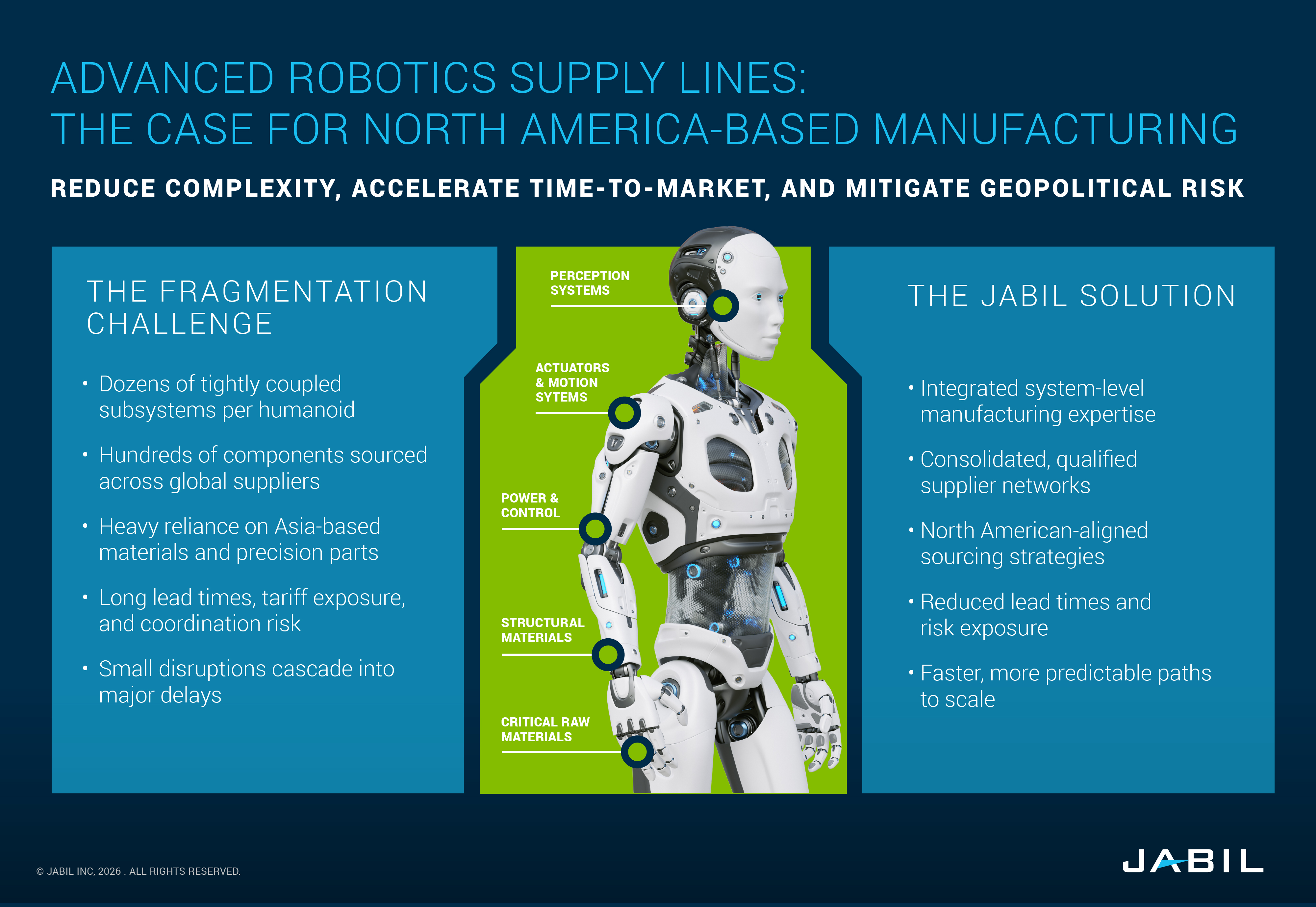

The manufacturing requirements for advanced robotics — particularly humanoid systems — introduce a level of complexity that extends well beyond conventional production platforms. At a systems level, a humanoid integrates two tightly coupled architectures: a “brain” built around high-performance compute, memory, and software, and a “body” composed of motion, sensing, and structural subsystems. The body alone requires dozens of actuators to achieve human-like degrees-of-freedom, with each actuator assembly combining precision motors, reducers, screws, bearings, encoders, and force sensors. These are not commodity parts. They demand tight tolerances, controlled calibration environments, and rigorous validation protocols to ensure repeatable performance under load.

Sensors — including vision, force/torque, inertial, and environmental sensors — must be integrated and calibrated to operate as a synchronized perception layer. Power systems, battery modules, thermal management, and wiring architectures must support high energy density while maintaining reliability and safety. Structural elements increasingly rely on advanced lightweight materials to balance strength, weight, and efficiency.

Producing these subsystems at scale requires embedded manufacturing engineering capability: precision assembly cells, actuator testing and break-in procedures, end-of-line validation systems, and continuous process optimization. Resilient supplier networks are equally critical which are in many cases the same partners serving automotive, aerospace, and advanced industrial supply chains.

Standing up both dimensions independently — plant-level engineering depth and globally coordinated supply lines — compounds capital intensity and extends time-to-scale. The challenge is not simply building a facility; it is building the operational ecosystem required to manufacture complex, multi-domain robotic systems reliably and repeatedly.

Jabil’s work across automation verticals — from AMRs and warehouse robotics to humanoids and drone platforms — reflects sustained investment in precisely this type of infrastructure. The engineering scale, supplier relationships, and cross-industry manufacturing intelligence that result from serving multiple sectors and product applications are difficult for a single OEM to replicate quickly or economically.

For OEMs whose differentiation lies in operating systems, AI models, and application-specific IP, aligning with an established manufacturing partner allows capital to remain focused on innovation and commercialization rather than duplicating industrial capability.

3. Geographic Optionality: It Is Not a Binary Choice

Perhaps the most persistent misconception among OEMs evaluating North American manufacturing is that the choice is binary: full U.S. production, or Mexico. In reality, the most effective strategies are deliberately architected networks that use both. The labor and investment dynamics of the current moment make getting this architecture right more consequential than ever.

At the end of 2025, the number of U.S.-based warehousing and storage employees fell to 1.85 million workers, according to preliminary data from the Bureau of Labor Statistics, the lowest count in the sector since November 2021, a period when employment across many industries was still recovering from pandemic-era disruption. Physically demanding roles in fulfillment, sorting, and last-mile preparation continue to see high turnover and chronic vacancies. The work that humans find hardest to sustain at scale is precisely the work that automation performs with consistency and without fatigue.

The same pressures apply across all the end markets served by robotics and automation systems. Restaurants and food service operations are deploying automated kitchen equipment and delivery robots to offset staffing shortfalls. Retailers are expanding autonomous inventory and checkout systems for the same reason. Last-mile delivery platforms are accelerating investment in drone and autonomous vehicle programs as driver availability and cost continue to constrain growth. The demand signal for automation is being generated from every direction simultaneously, and the OEMs positioned to meet it at scale are the ones who have already solved their manufacturing equation. The question is how to meet it efficiently.

Full U.S. production carries a cost premium, particularly for labor-intensive assembly. But it also offers genuine advantages: direct proximity to customers, faster response to design iteration requests, and alignment with Made in America sourcing commitments that increasingly matter to retail partners and investors alike.

Mexico-based production in established manufacturing hubs like Chihuahua and Guadalajara, which have deep experience in complex electronics and electromechanical assembly, offers compelling cost efficiency without sacrificing access to the U.S. market, provided USMCA rules are properly applied.

And capabilities are growing. What began as high-volume, low-mix production has evolved into a genuinely competitive environment for technology-rich, precision-dependent product categories, exactly the profile of advanced robotics hardware. By 2023, Mexico had surpassed mainland China as the largest goods exporter to the United States, reflecting years of sustained investment in manufacturing infrastructure, workforce development, and supply chain sophistication. That trajectory is accelerating as nearshoring initiatives continue drawing technically complex production work from Asia into Latin America.

A 2024 Bain & Company report confirms the momentum taking hold this decade: 81% of CEOs and COOs are actively planning or executing moves to bring supply chains closer to home markets, with 64% actively investing in reshoring or nearshoring. But notably, only 2% had fully completed that transition, underscoring just how much ground remains to be covered.

Manufacturing networks that intentionally combine U.S. engineering depth and customer proximity with Mexico-based production scale create built-in strategic flexibility. This geographic optionality allows OEMs to respond to market shifts, tariff changes, or demand fluctuations without restructuring entire supply chains. The companies that design for this flexibility from the start are measurably better positioned than those who arrive at it reactively.

Closing the North American Deployment Gap

Taken together, these three barriers — regulatory complexity, capital intensity, and geographic strategy — explain why automation and robotics deployments have expanded more slowly than the market opportunity would suggest. The gap from strategic intent to operational execution is real, but it is also closable, and the OEMs doing it successfully share a recognizable approach.

They have stopped trying to solve these challenges independently. They have found manufacturing partners who bring regulatory intelligence, existing infrastructure, engineering depth, and a diverse geographic footprint to the table, allowing them to accelerate their path to scale while preserving the capital flexibility needed to keep innovating.

In North America, where the conditions for a major scaling moment in robotics and automation are now fully in place, the companies that move with purpose and the right partners will build advantages that compound over time.

The market is not waiting. The labor shortage is not abating. The technology is not standing still. The only variable still in play is how quickly your organization is ready to move.

How can Jabil help solve your automation and physical AI challenges?

Get in touch.